This post will explain you why you should avoid ULIPs and endowment insurance and what to choose for instead.

ULIPs and endowment plans are quite popular in India. Most consumers, either deliberately or unknowingly, purchase one of these two types of policies. They look to be straightforward, transparent, and really useful. This post is a genuine attempt by us to remove the mystique (or should we say hype?) around ULIPs and endowment plans. We will also advise you about the finest options.

What are ULIPs and Endowment plans?

They are both insurance and investment products. Neither is advised since they provide a suboptimal combination of insurance and investment.

Endowment plans provide a guaranteed payout known as the amount assured, whilst ULIPs are market-linked insurance schemes that invest in equities or debt-oriented schemes.

Why are they so popular?

Three reasons came to our mind and we think you will agree with at least one of the reasons.

- Many Indians acquire insurance in haste, mostly for the goal of saving taxes, and do so without fully comprehending the goods.

- Often, the insurance agent is a neighbor, an acquaintance, or, worse, a family member. It’s difficult to turn them down. As a result, we purchase an endowment or ULIP without much deliberation. Agents also strongly advocate for these policies since they provide substantial compensation.

- Many individuals consider insurance to be an unnecessary cost, and hence believe it is preferable to simply purchase a product that will provide some return. They fail to recognize the influence of inflation, as well as the suboptimal returns from these items.

What’s wrong with them?

Neither do they provide adequate insurance, nor a good investment solution. Let’s explore the point by looking at the two purposes separately.

Insurance

Most people don’t understand what sort of insurance coverage they require. For example, in a family of four, when you are the sole earner, a life insurance policy of Rs 5 lakh (see example below) is just insufficient in the case of your untimely death. The effect is more severe if you haven’t given them much inheritance and/or have outstanding loans. In addition, inflation will chip away at your money. To put things in perspective, if a term plan with a cover of Rs 50 lakh costs Rs 7000 per year, a ULIP will cost you Rs 5 lakh.

Investment

The excessive costs are the most significant disadvantage. A large portion of the premium you pay, especially in the early years, is withdrawn in the form of different fees and levies, the most significant of which is distributor commissions. This decreases how much of your premium is really invested to create profits. Over time, this has a significant influence on the amount of money you may build. We have highlighted one component of ULIP, namely the multiple charges.

ULIP

Age: 35

Annual premium: Rs 50,000

Sum Assured: Rs 5,00,000

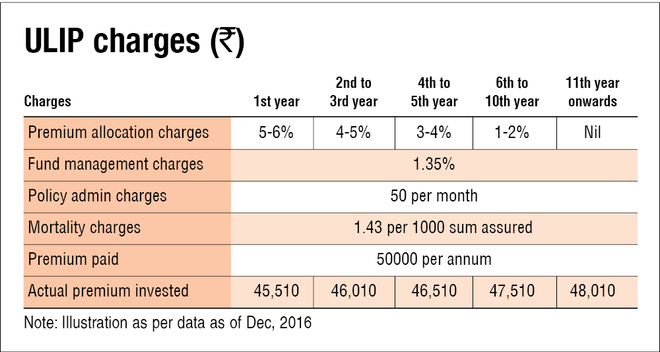

The table below enlists a set of charges that are levied by ULIPs. Now, mind you that these charges aren’t exactly hidden. You will find them on your policy papers but probably wouldn’t give it much importance. The actual invested amount is after deducting the following charges which make up almost 7% of the total invested amount.

So, in 10 years you have paid Rs 5 lakh. However, the actual invested amount, after deducting all the aforementioned charges, will be around Rs 4.68 lakh.

So what are the alternatives?

It is always better to keep insurance and investment separate. If you have financial dependents, the first thing that you should do is to buy a term insurance with an adequate cover. Put the rest of the money in one or two good diversified equity funds. But, what if you are risk averse? In that case, we would suggest you to stick to a term plan & good old PPF. It will still give you better returns than an endowment plan.

A number is worth a thousand words

We don’t want you to take our word (or anyone else’s for that matter) for it. So, let’s examine the shortcomings through an illustration.

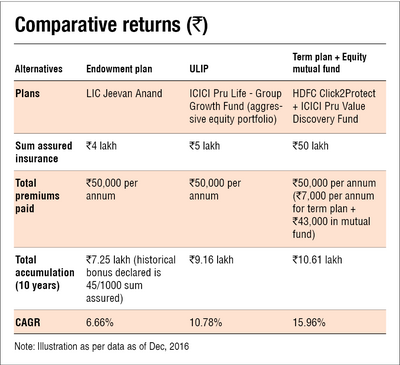

In the table, we have taken the 3 possible options – buying a ULIP, buying an endowment plan, and buying a term plan+equity mutual fund. The table illustrates what kind of returns you would get on each in the last 10 years (based on historical data). For the sake of parity and returns, we have considered the best performing products from each category.

Inference

The table above is rather self-explanatory. First, the third choice provides ten times higher insurance coverage (50 lakhs) than a ULIP. Secondly, the third alternative provides a much higher return. So far, the judgment appears to be obvious.

Advice

Insurance is a cost, and should be addressed as such. Don’t combine insurance with investing. Combining the two will result in less than average profits on both.