The distinctions between liquid funds and overnight funds are too narrow. In such cases, when should these monies be used? Are both of these categories safe? What are the hazards involved?

Liquid Funds and Overnight Funds are regarded as the most safe parking mechanisms. However, many people are unsure when to employ liquid funds vs overnight funds. In such a case, it is best to first grasp the fundamentals of these two types of debt funds in depth.

What do you mean by Overnight Funds?

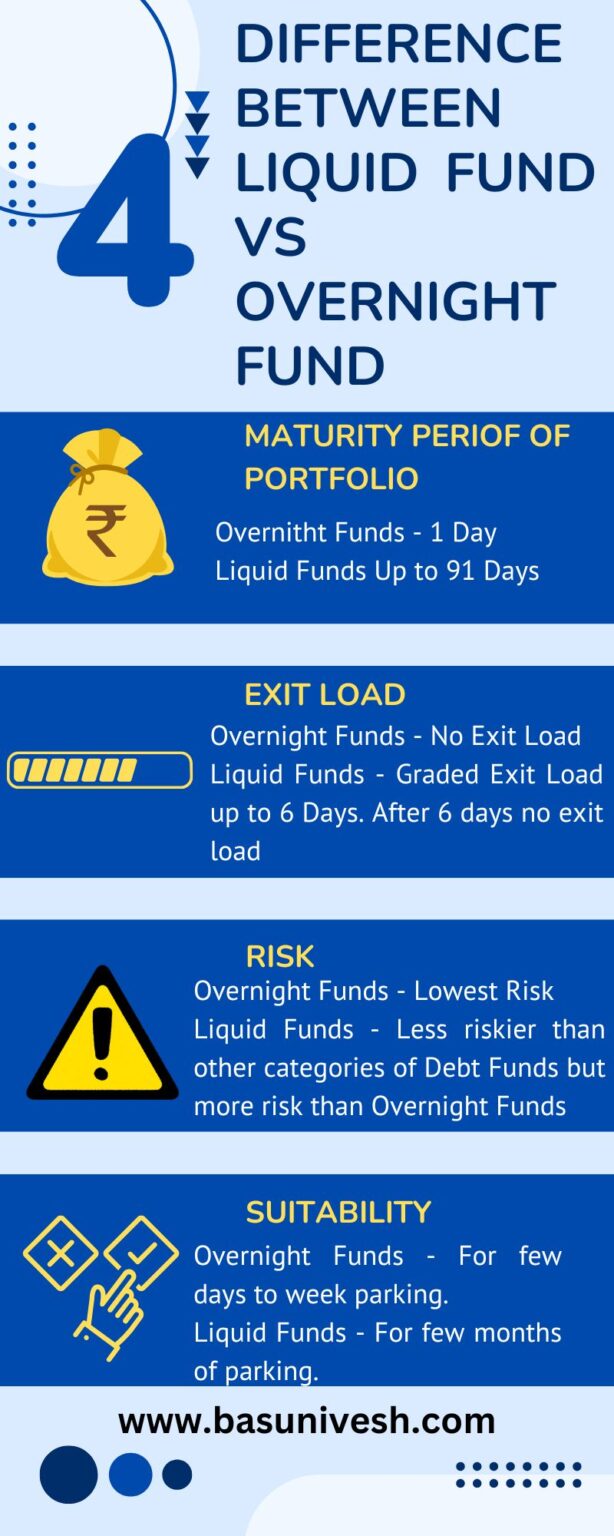

An overnight mutual fund invests largely in bonds with the shortest maturity period, namely one day. As a result, its portfolio consists mostly of cash and is exposed to daily changes. Although the possibility for capital loss in this category is lower than in other mutual funds, investors should be aware of the additional risks connected with these investments.

Many people believe Overnight Funds to be the safest option among all debt funds due to the underlying assets’ short maturity duration of only one day. However, there is a level of risk known as REINVESTMENT RISK that should not be underestimated.

It is vital to emphasize that this presents no threat to your principal. However, as you are aware, any changes made by the Reserve Bank of India (RBI) to its reverse repo rate may lessen the attraction of investing short-term funds with the RBI. In these conditions, investors who use overnight funds, which are intended for short-term investments, may notice lower returns, but this does not mean a loss of capital. As a result, before investing in Overnight Funds, you must first comprehend their predicted returns.

Overnight Funds are an ideal alternative for temporarily keeping extra cash for durations shorter than a week because they do not levy an exit fee. However, like with typical bank fixed deposits, the returns are subject to taxes based on your applicable tax band.

Overnight money’ primary advantage over Bank Fixed Deposits is its liquidity, which allows access to money anytime needed without paying any early penalties or exit costs.

DO NOT EXPECT MORE THAN YOUR SAVINGS ACCOUNT’S INTEREST RATE FROM OVERNIGHT FUNDS!!

What do you mean by Liquid Funds?

Liquid funds invest in assets with maturity periods of up to 91 days. As a result, these funds face larger risks from interest rates, credit, and defaults than Overnight Funds, which often have money returned the next day when the Fund Manager’s holdings mature.

Liquid Funds impose a graded exit burden for up to six days (Day 1: 0.0070%, Day 2: 0.0065%, Day 3: 0.0060%, Day 4: 0.0055%, Day 5: 0.0050%, and Day 6: 0.0045%), after which there is no exit load beginning on the seventh day. These funds can invest in a variety of money market securities, including Certificates of Deposit (CDs) and Commercial Papers (CPs), with maturities of up to 91 days, independent of credit quality. As a result, they may incur a bigger credit risk than Overnight Funds.

Liquid Funds have more flexibility in controlling credit risk since their portfolios are longer in maturity, which often leads in higher returns than Overnight Funds. If you need money right now, Overnight Funds are a better alternative. Liquid Funds, on the other hand, are the best option if you want to make returns while retaining extra funds for more than a week.

As previously stated, liquid money do not ensure perfect protection. There have been instances in the past where the net asset value (NAV) of liquid funds fell by approximately 7% in a single day. (See my previous writings “Is Liquid Fund Safe and an Alternative to Savings Account?” and “Should We Invest in Liquid Funds for Long Term Goals?”).

Otherwise, to learn more about the hazards of debt mutual funds, check out my “Debt Mutual Funds Basics” series of articles.

Remember that certain Liquid Funds allow quick redemption, however it is restricted to Rs.50,000 or 90% of the invested amount, which is sent to your bank account within 30 minutes. Also, not all mutual funds would provide such fast redemption options. Liquid Funds are taxed in the same way that traditional Debt Mutual Funds are (based on your tax bracket). Refer to my most recent post on “Budget 2024 – Mutual Fund Taxation FY 2024-25 / AY 2025-26”.

Liquid Funds Vs Overnight Funds Difference – When to use them?

You now have a comprehensive knowledge of both types of debt funds. According to our observations, the taxation of various debt fund categories is similar to that of bank fixed deposits, depending on your tax bracket. Furthermore, one should not expect returns that surpass the interest rate on a savings account for overnight funds or the short-term fixed deposit rate for liquid funds. Given this environment, what role should liquid funds or overnight funds play, and when should they be used?

Overnight cash are suited for circumstances requiring cash for a period of less than one week. Liquid Funds, on the other hand, are better suited for short-term funding requirements. If you know when you’ll need the money, traditional bank fixed deposits (FDs) are a good option. There is no need to complicate your choice between Overnight and Liquid Funds if your needs are simple. If you are unsure about the timeliness of your financial demands in a short period of time, you can choose either Overnight Funds or Liquid Funds. If you have a sweep-in Bank FD, it is highly suggested that you prioritize it over the other debt fund types described above.

I hope this has cleared up any confusion about the difference between liquid funds and overnight funds, and when to use them. For convenience, you may also refer to the illustration below.